As of 01/01/2020, a receipt must be issued for all business transactions and handed out in which a third party is involved.

The following regulations have to be observed:

- The receipt has to be issued immediately after the completion of the transaction.

- The receipt may be provided in electronic form - with the client's consent - or in paper form.

- The client does not have to take or retain the receipt. The issuer of the receipt is not obliged to retain receipts that have not been taken.

- An electronic receipt must be issued in a standardised data format (e.g. JPG, PNG or PDF) so that the customer can read the receipt with a free standard software.

- In individual cases, for reasons of reasonableness, an exception to the document output obligation can be applied for or granted by the authorities in accordance with § 148 AO.

- On a voluntary basis, a QR code can (also) be printed, which makes it much easier and faster to check the receipt.

Receipt requirements

All required information is regulated in the KassenSichV. All information are obliged to be legible to anyone without machine assistance and have to be contained on the paper receipt or in the electronic receipt.

The receipt has to contain the following information:

- Full name and address of the supplying / issuing company.

- Date of issue of document and time of commencement and completion of transaction

- Quantity and nature of the service/items

- transaction number

- remuneration and the amount of tax due on it or reference to tax exemption

- the logged serial number

- Amount per payment type

- signature counter

- test / verification value

Optional: QR-code containing TSS / TSE data

The main purpose of the obligation to issue receipts and the security elements is that it is easy to check whether all business transactions have been correctly recorded in the event of a cash register inspection / audit.

Since July 2021, it is no longer necessary to print the TSE data in plain text on the receipt. In its 1006th plenary session on 25/06/2021, the German Bundesrat had passed an amendment to the Cash Security Ordinance. Specifically, §6 sentence 2 of the KassenSichV - "Requirements for the receipt" was amended:

"The information on a receipt pursuant to sentence 1 must be legible to anyone without machine assistance or readable on a QR code."

See also news article on the RetailForce website: https://www.retailforce.cloud/bundesrat-beschliesst-aenderungen-an-kassensichv/

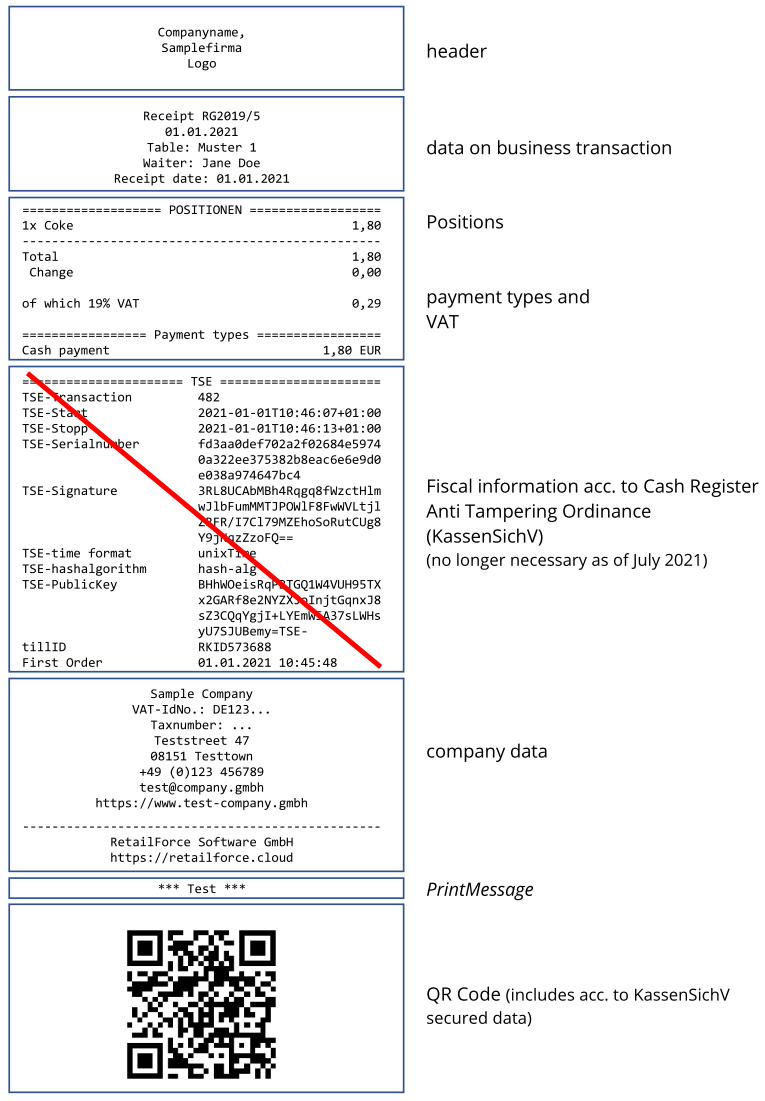

Example of receipt:

Elements

| header | Contains header information such as company name and address, logo etc. |

| data on business transaction |

contains for example

|

| positions and payment information | information on all items sold, payment type, VAT as well as totals and grand total |

| fiscal information |

Fiscal information acc. to Cash Register Anti Tampering Ordinance. No longer necessary as of July 2021 - information can be displayed in the form of the QR code. |

| company data |

official information on the company issuing the receipt, like name, address, contact information,... |

| PrintMessage |

Part of FiscalResponse from Fiscal Client - has to be printed on the receipt |

| QR Code* |

contains fiscal information; edge length min. 3cm, quality: min. 300dpi recommended. Error correction level during creation recommended |

* Version 2.3 of the DSFinV-K indicates a shortened inspection if the receipt contains a QR code.

Quote: "If the receipt contains a QR code, a cash register inspection can possibly already be completed if the receipt verification functions and the integrity and authenticity of the records can be checked by the authorised officer with individual receipts." [translated from the original German text] (Cf. DSFinV-K v2.3, Annex I, p. 120).

Comments

0 comments

Please sign in to leave a comment.